High Yield USDC Savings via Mobile Money in Nigeria and Kenya 2026

In the bustling markets of Lagos and the vibrant streets of Nairobi, a financial revolution is quietly unfolding. As of February 2026, USD Coin (USDC) holds steady at $1.00, providing a rock-solid anchor for savers battered by relentless inflation. Platforms like Risevest and Bamboo in Nigeria are delivering annual returns of 12% to 15% on USDC holdings, while Kenya’s M-Pesa ecosystem is bridging stablecoins to everyday mobile money, slashing remittance costs and unlocking high-yield opportunities. This isn’t hype; it’s a fundamental shift toward sustainable wealth preservation in Africa’s digital economy.

Navigating Nigeria’s Inflation Storm with USDC Savings

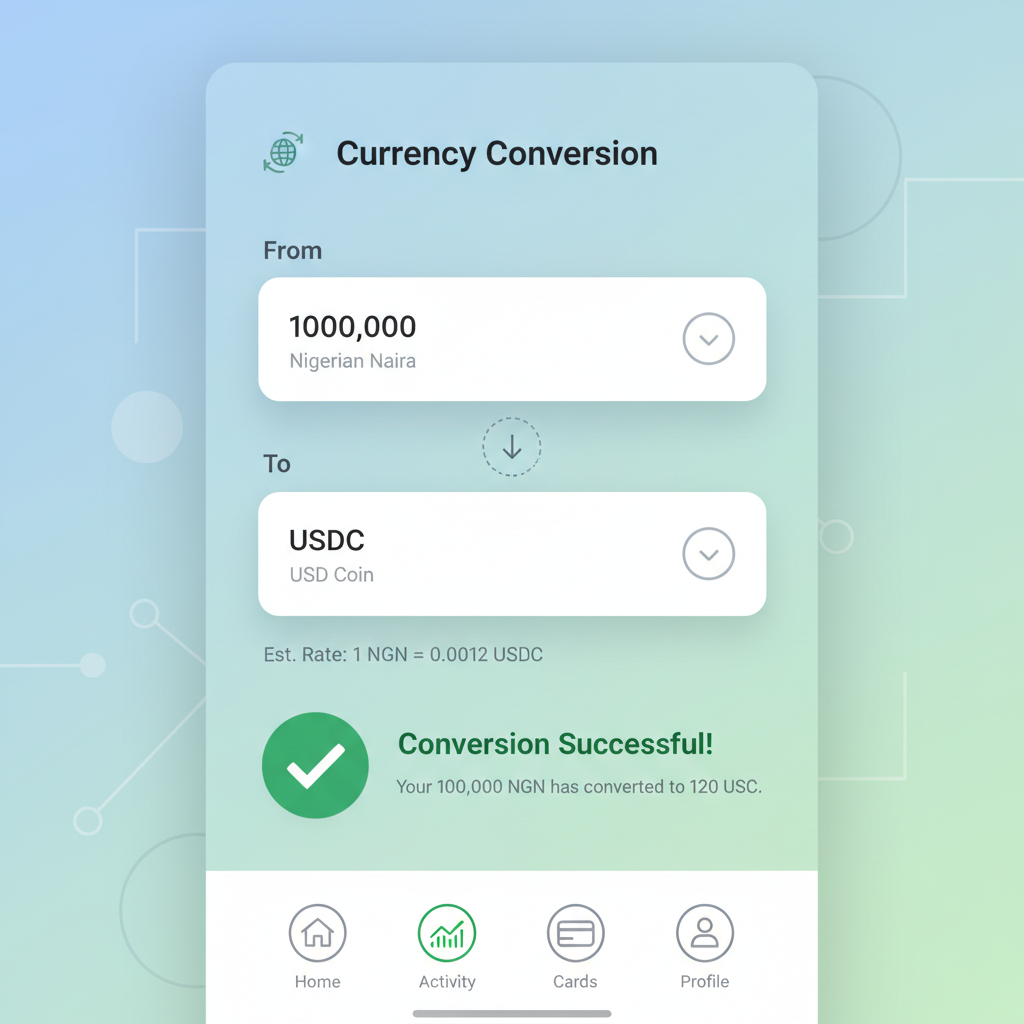

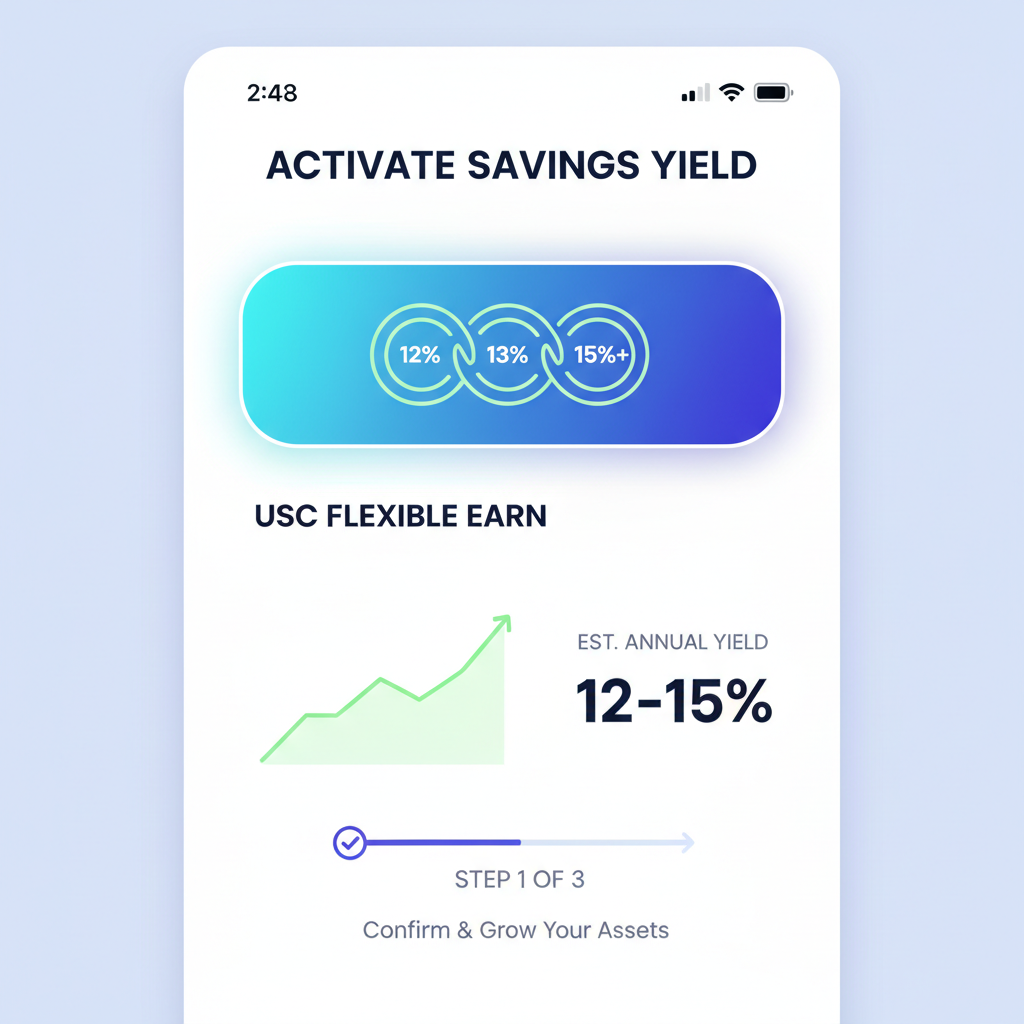

Nigeria’s naira has long been a casualty of macroeconomic turbulence, prompting savvy savers to flock to stablecoins. USDC savings mobile money Nigeria setups are now mainstream, with fintechs channeling funds into U. S. real estate for those compelling 12-15% yields via Risevest. Bamboo complements this by offering 8% on USD wallet balances, a passive income stream that outpaces traditional banks. I view this as a masterstroke in capital allocation: time in stable, dollar-pegged assets trumps chasing volatile local yields.

Consider the mechanics. Users deposit via MTN MoMo or bank transfers, converting seamlessly to USDC at $1.00. Yields accrue daily, compounded without the drag of currency devaluation. Platforms like Busha Earn set the benchmark at 7.5%, but 2026 innovations promise even more. This integration sidesteps P2P marketplace risks, favoring regulated on-ramps that prioritize security and liquidity.

Stablecoins like USDC are leapfrogging Africa’s legacy banking, turning mobile phones into high-yield vaults.

Kenya’s M-Pesa Evolution: High Yield Stablecoin Savings Unleashed

Across the border, high yield stablecoin savings Kenya is synonymous with M-Pesa’s blockchain pivot. The partnership with ADI Foundation deploys USDC infrastructure for instant cross-border flows, converting shillings to USDC at $1.00 and back with minimal fees. Mobile money operators report treasury windfalls, like $900k in extra income from stablecoin strategies, some passed directly to users as boosted savings rates.

Stablecoin savings M-Pesa users now access DeFi-grade products: high-yield deposits rivaling 10% and, lending pools, and asset management. Yellow Card’s insights reveal how these operators monetize idle floats, extending benefits to everyday remitters. From Nairobi traders to Kenyan diaspora, USDC yields Africa mobile wallet access democratizes returns once reserved for the elite.

This convergence addresses core pain points: volatility, high fees, and sluggish transfers. In my 18 years as an investor, I’ve seen few innovations match stablecoins’ blend of stability and growth potential.

Why USDC Stands Out in Mobile Money Ecosystems

USDC deposit MTN MoMo Africa and similar ramps via Paychant exemplify frictionless fiat-stablecoin bridges. Regulated fintechs dominate acquisition channels, blending P2P efficiency with compliance. Plasma’s analysis underscores Nigeria’s stablecoin surge, mitigating inflation while fueling digital economies.

VALR-Mukuru’s South African model hints at regional scalability, with USDC payments, storage, and yields integrating into wallets continent-wide. Bitso’s take on emerging markets rings true: stablecoins solve cross-border headaches, from remittances to trade settlements.

USD Coin (USDC) Price Prediction 2027-2032

Forecasts emphasizing peg stability amid surging adoption in high-yield mobile money savings in Nigeria and Kenya

| Year | Minimum Price | Average Price | Maximum Price | YoY % Change (Avg) |

|---|---|---|---|---|

| 2027 | $0.98 | $1.00 | $1.02 | 0.00% |

| 2028 | $0.99 | $1.00 | $1.01 | 0.00% |

| 2029 | $0.99 | $1.00 | $1.01 | 0.00% |

| 2030 | $0.995 | $1.00 | $1.005 | 0.00% |

| 2031 | $0.997 | $1.00 | $1.003 | 0.00% |

| 2032 | $0.998 | $1.00 | $1.002 | 0.00% |

Price Prediction Summary

USDC is projected to robustly maintain its $1.00 peg through 2032, with narrowing min/max ranges reflecting enhanced stability from African market adoption, improved reserves, and regulatory clarity. Bearish mins account for potential short-term depegs during global stress; bullish maxes for demand surges from remittances and yields (10-18% APY).

Key Factors Affecting USD Coin Price

- Massive stablecoin adoption via M-Pesa, Mukuru, Risevest, and Bamboo in Nigeria/Kenya driving demand.

- Regulatory advancements supporting stablecoins in emerging markets, reducing depeg risks.

- High-yield savings (10-18% APY) integration with mobile money boosting USDC utility and liquidity.

- Circle’s reserve transparency and audits ensuring long-term peg integrity.

- Competition from USDT but USDC’s compliance edge in regulated fintechs.

- Global USD strength, market cycles, and blockchain upgrades influencing minor fluctuations.

- Cross-border remittance efficiency lowering fees and volatility exposure.

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis.

Actual prices may vary significantly due to market volatility, regulatory changes, and other factors.

Always do your own research before making investment decisions.

Fundamentally, USDC’s $1.00 peg, backed by reserves, ensures predictability. Savers earn without principal erosion, a rarity in high-inflation zones. As adoption scales, expect yields to stabilize around sustainable levels, rewarding patience over speculation.

Binance notes the M-Pesa-USDC synergy, with Nigerians and Kenyans leading the charge. This mobile-first approach positions Africa as a stablecoin powerhouse, where high yields meet accessibility.

Hashed Emergent’s Substack captures this leapfrogging perfectly: platforms like Busha Earn deliver up to 7.5% on stablecoins, outstripping local savings accounts eroded by inflation. Yet, as yields climb toward 10-18% in projections, the real edge lies in platforms engineered for Africa’s mobile-first reality.

Unlocking Everyday Wealth: Practical Steps for USDC Deposits

USDC deposit MTN MoMo Africa setups, alongside M-Pesa ramps, make entry straightforward. Fintechs like Paychant handle conversions from local currencies to USDC at its unwavering $1.00 peg, ensuring no slippage from volatility. In my experience, the key to enduring returns is consistent deposits into compounded yield products, bypassing the feast-or-famine cycle of traditional finance.

Master High-Yield USDC Savings: Mobile Money Deposits in Nigeria & Kenya

Once onboarded, users tap into treasury-backed yields without counterparty gambles. Mobile money operators, per Yellow Card, have unlocked $900k in risk-free income, trickling benefits to savers via competitive APYs. This isn’t speculative DeFi; it’s prudent allocation to audited reserves, yielding steady growth.

For Nigerian hustlers and Kenyan entrepreneurs, these tools mean remittances arrive as USDC at $1.00, instantly deployable into savings. No more wiring fees devouring 10% of transfers. Instead, funds compound, building buffers against naira or shilling slides.

Balancing Rewards with Realities: Risks in Focus

High yields tempt, but thoughtful investing demands scrutiny. Platform solvency tops the list; opt for regulated entities like those partnering with Circle for USDC issuance. Smart contract exploits in DeFi extensions pose risks, though core savings products minimize exposure. Regulatory flux in Nigeria and Kenya warrants vigilance, yet bodies like the Central Bank of Nigeria signal openness to stablecoins as inflation hedges.

Currency peg breaks are rare for USDC, audited monthly to affirm its $1.00 backing. Counterparty risk fades with direct Circle integration, unlike opaque P2P trades. My CFA lens prioritizes platforms stress-testing yields against reserve rates, ensuring sustainability over flashy APYs destined to falter.

Patience compounds; chasing peaks erodes principal. Stick to USDC’s proven peg for Africa’s wealth builders.

AfricaStableSave. com exemplifies this rigor, tailoring USDC products for mobile money users across Nigeria and Kenya. Seamless MTN MoMo and M-Pesa bridges deliver 12-15% yields via diversified U. S. assets, with off-ramps matching inbound efficiency. No lockups, daily compounding, and 24/7 access define its edge.

Plasma. to charts Nigeria’s stablecoin ascent, paralleling Kenya’s M-Pesa dominance. As ADI Foundation rollouts expand, cross-border trade flourishes, with USDC settling deals at $1.00 parity. Mukuru-VALR’s blueprint scales north, promising uniform yields from Cape Town to Lagos.

Worldwide Stablecoin Payment Network’s DeFi suite, deposits, lending, integrates natively, amplifying returns. Bitso’s emerging markets playbook confirms: stablecoins cut remittance frictions, fueling intra-African commerce. For savers, this means portfolios resilient to local shocks, growing methodically.

Africa’s digital natives grasp this intuitively. From diaspora funds parked in USDC savings mobile money Nigeria accounts to Nairobi vendors stacking high yield stablecoin savings Kenya pots, adoption surges. Platforms evolve, yields refine, yet the principle endures: anchor to dollars, harvest growth. AfricaStableSave. com stands ready, bridging wallets to wealth in this stablecoin era.