Africa's savers face a relentless foe: inflation that gnaws at bank deposits like termites through wood. In Nigeria, the naira has shed over 50% of its value in recent years; Ghana's cedi fares no better, while Kenya's shilling stumbles amid volatile forex swings. Traditional banks offer paltry yields, often below 5%, leaving depositors to watch their purchasing power evaporate. USDC savings Africa mobile money flips this script, channeling dollar-pegged stability directly into users' phones via platforms like AfricaStableSave. com. This fusion of stablecoins and ubiquitous mobile wallets delivers inflation proof savings USDC Africa desperately needs, with yields that actually grow wealth.

Stablecoins are rapidly emerging as a critical financial tool for everyday users seeking protection against currency depreciation. (Source: The Tribune)

Africa's Inflation Crisis Devours Traditional Savings

Consider the numbers: sub-Saharan Africa's average inflation hovers above 15%, spiking to hyperinflation levels in hotspots like Zimbabwe and Sudan. Bank deposits, touted as safe havens, yield a fraction of that erosion rate. A Nigerian trader parking 100,000 naira at 4% interest watches it lose real value as prices climb 25% annually. Remittances, a lifeline for millions, arrive devalued through leaky forex channels. Sources like Garowe Online report millions turning to stablecoins as shields against this chaos, bypassing fragile local currencies.

Institutional voices echo this shift. Fireblocks notes retail Africans already favor USDT and USDC to combat hyperinflation, with Nigeria, Ghana, and Kenya leading adoption. Vera Songwe on LinkedIn highlights how these digital dollars serve practical needs - moving value, not speculating. Yet banks cling to outdated models, their deposits a trap for the unwary.

This vulnerability drives innovation. Platforms like Yellow Card and Chipper Cash integrate USDC with M-Pesa and other mobile money systems, letting users convert local earnings to stable value in seconds. No foreign accounts required, just a phone - perfect for freelancers dodging naira plunges or Kenyan remitters slashing fees.

USDC on Mobile: Seamless Access to Dollar Power

USDC stands out in this arena, fully backed 1: 1 by U. S. dollars and equivalents, regulated under U. S. frameworks for trust. Unlike volatile cryptos, it holds steady, preserving capital amid turmoil. AfricaStableSave. com pioneers mobile wallet USDC yields Africa, enabling deposits from mobile money, automatic yield accrual, and off-ramps to local fiat. Strategic macro trends favor this: as U. S. rates stay elevated, USDC savings products offer 5-10% APY, dwarfing bank rates.

Sendwave explains how stablecoins like USDC track the dollar, hedging high-inflation woes. Quona Capital adds they thrive with mobile agents, no bank needed. In Nigeria, Plasma. to observes users flock to USDC for digital dollar storage, evading devaluation. This isn't hype; it's pragmatic finance leapfrogging creaky systems, as Hashed Emergent argues, with yields beating savings accounts continent-wide.

Challenges linger - regulatory fog in some markets, education gaps - but momentum builds. Freelancers convert gig earnings to USDC instantly; traders hedge forex risks. AfricaStableSave streamlines this, optimizing for continental digital economies.

High-Yield Edge: Stablecoin Savings Crush Bank Alternatives

High yield stablecoin savings Africa isn't just buzz; it's math. Bank fixed deposits top out at 7% in best cases, often eroded by fees and taxes. USDC products via mobile? Compounded yields from DeFi protocols hit double digits, risk-adjusted for stability. AInvest details sub-Saharan reshaping via stablecoins, pragmatic against hyperinflation. Center for Global Development warns they challenge public finances but empower individuals.

Picture a Ghanaian small business owner: 1,000 cedis in bank shrinks real terms; same in USDC grows via yields, redeemable to mobile money anytime. AfricaStableSave tailors this, with seamless bridges ensuring liquidity.

USDC Price Prediction 2027-2032

Peg Stability and Yield Outlook for African Savers Using Mobile Money Amid Inflation

| Year | Minimum Price | Average Price | Maximum Price | Expected Yield Range (APY) |

|---|---|---|---|---|

| 2027 | $0.95 | $0.99 | $1.03 | 6-10% |

| 2028 | $0.97 | $0.995 | $1.02 | 7-11% |

| 2029 | $0.98 | $0.998 | $1.015 | 7-12% |

| 2030 | $0.985 | $1.00 | $1.01 | 8-12% |

| 2031 | $0.99 | $1.00 | $1.008 | 8-12% |

| 2032 | $0.992 | $1.00 | $1.005 | 8-12% |

Price Prediction Summary

USDC is expected to maintain its critical $1 peg through 2027-2032, with minor deviations in bearish (regulatory stress, depeg risks) and bullish (high African demand) scenarios. Increasing adoption as an inflation hedge via mobile money will ensure stability, supported by improving yields from 6-12% APY, far surpassing traditional bank deposits.

Key Factors Affecting USD Coin Price

- Massive adoption surge in Africa (Nigeria, Kenya, Ghana) for remittances and savings preservation

- Regulatory clarity and supportive policies for stablecoins in high-inflation markets

- Technological integrations with mobile money platforms like M-Pesa and Chipper Cash

- Circle's reserve management and transparency bolstering peg confidence

- Competition from USDT/USDi but USDC's compliance edge

- US interest rates and T-bill yields influencing APY offerings

- Potential volatility from global crypto cycles or bridge/chain-specific issues, though mainnet peg holds firm

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis. Actual prices may vary significantly due to market volatility, regulatory changes, and other factors. Always do your own research before making investment decisions.

Those projected yields aren't pie-in-the-sky; they're powered by DeFi protocols channeling real U. S. Treasury returns into everyday African wallets. While banks tout 'security, ' their low rates betray savers in inflation's grip. Stablecoin savings vs bank Africa reveals a stark divide: mobile USDC products compound at rates banks can't touch, all without the red tape of physical branches.

Why Mobile Money Bridges Unlock True Potential

Africa's 600 million mobile money users hold the key. Platforms fuse M-Pesa, MTN MoMo, and Airtel Money with USDC, turning airtime top-ups into yield-bearing assets. No spreadsheets needed; apps handle conversions at market rates, accruing interest passively. This setup suits hustlers from Lagos markets to Nairobi tech hubs, preserving freelance dollars before local currency bites. Hashed Emergent nails it: stablecoins leapfrog outdated finance, delivering superior returns precisely when traditional options falter.

Yet skeptics point to risks - peg breaks, hacks, regulation. History counters: USDC's transparency, with monthly attestations, outshines opaque banks. Nigeria's Plasma users prove it, storing digital dollars seamlessly. Regulatory tailwinds brew too; Kenya and Ghana eye frameworks favoring compliant stablecoins, per Vera Songwe's insights. For strategic savers, timing matters: lock in yields now as U. S. policy stabilizes dollar strength.

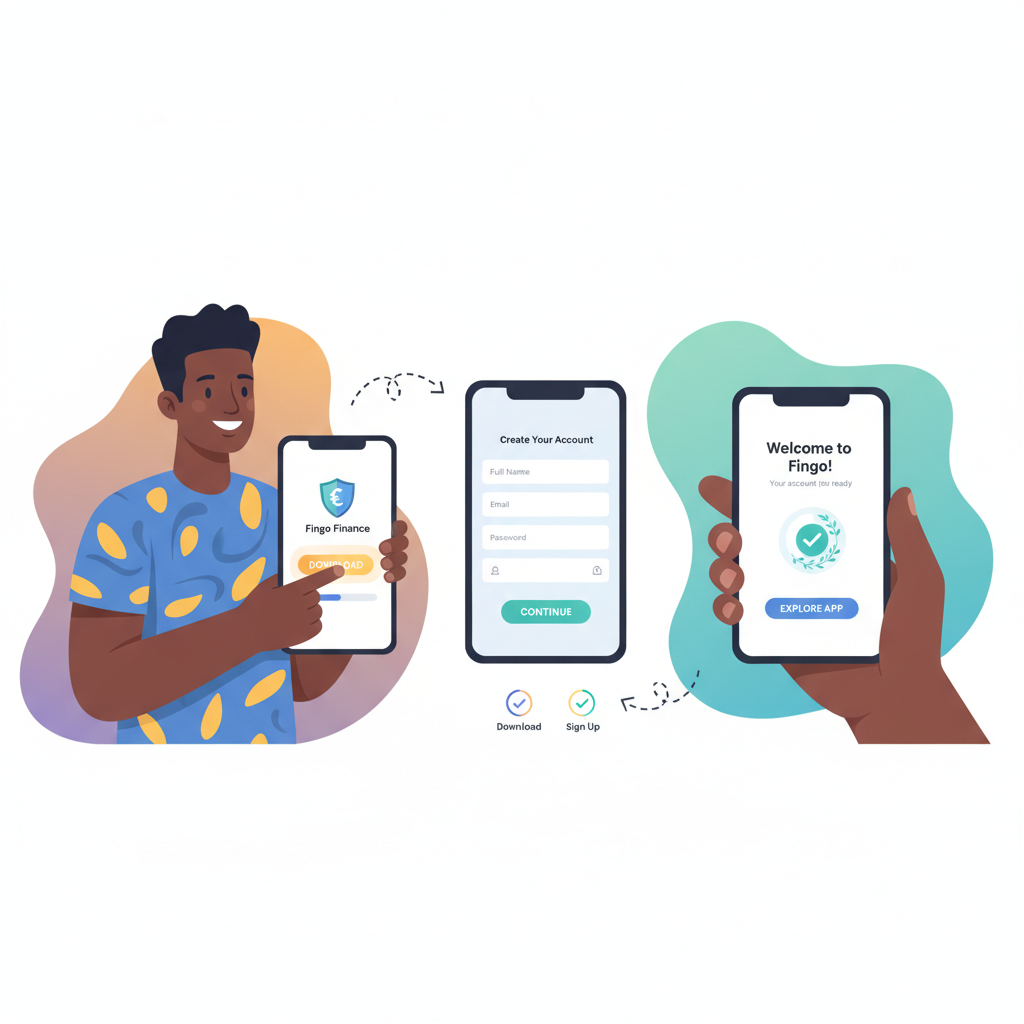

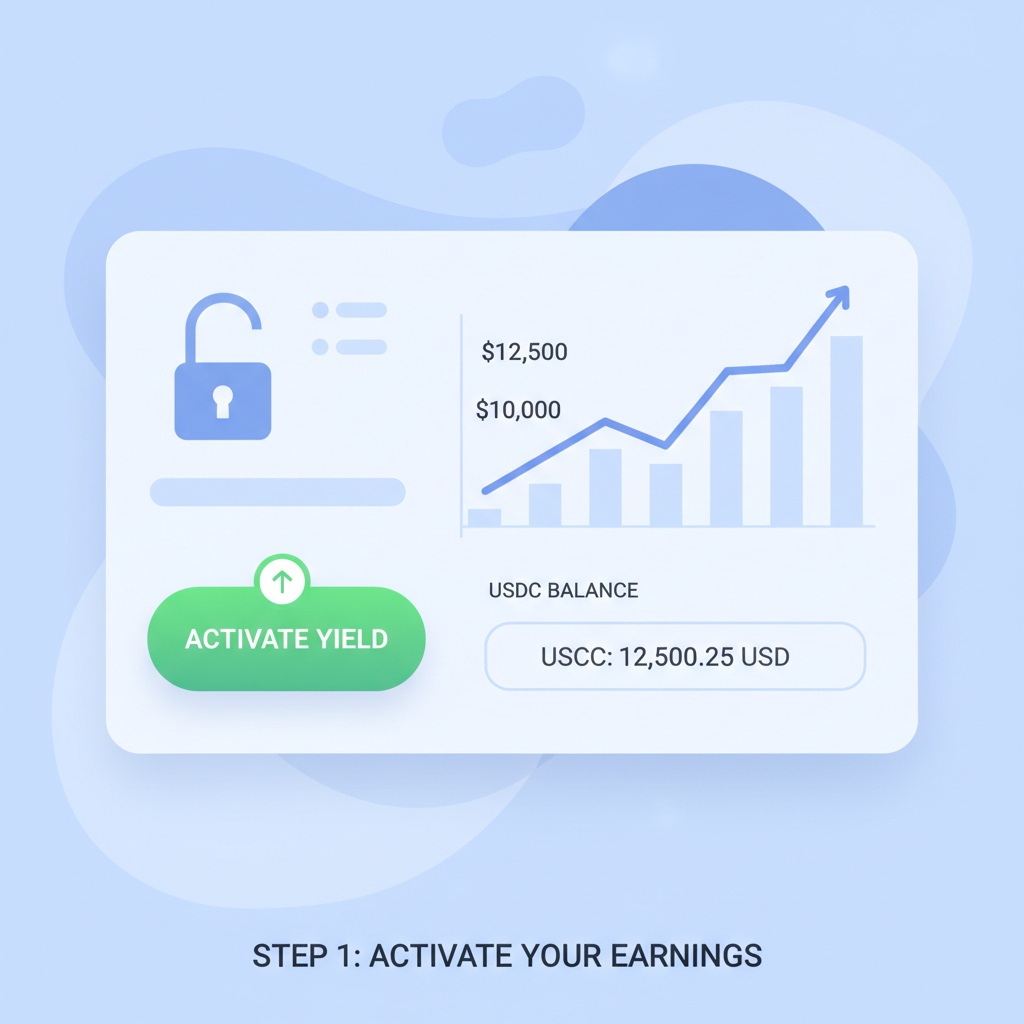

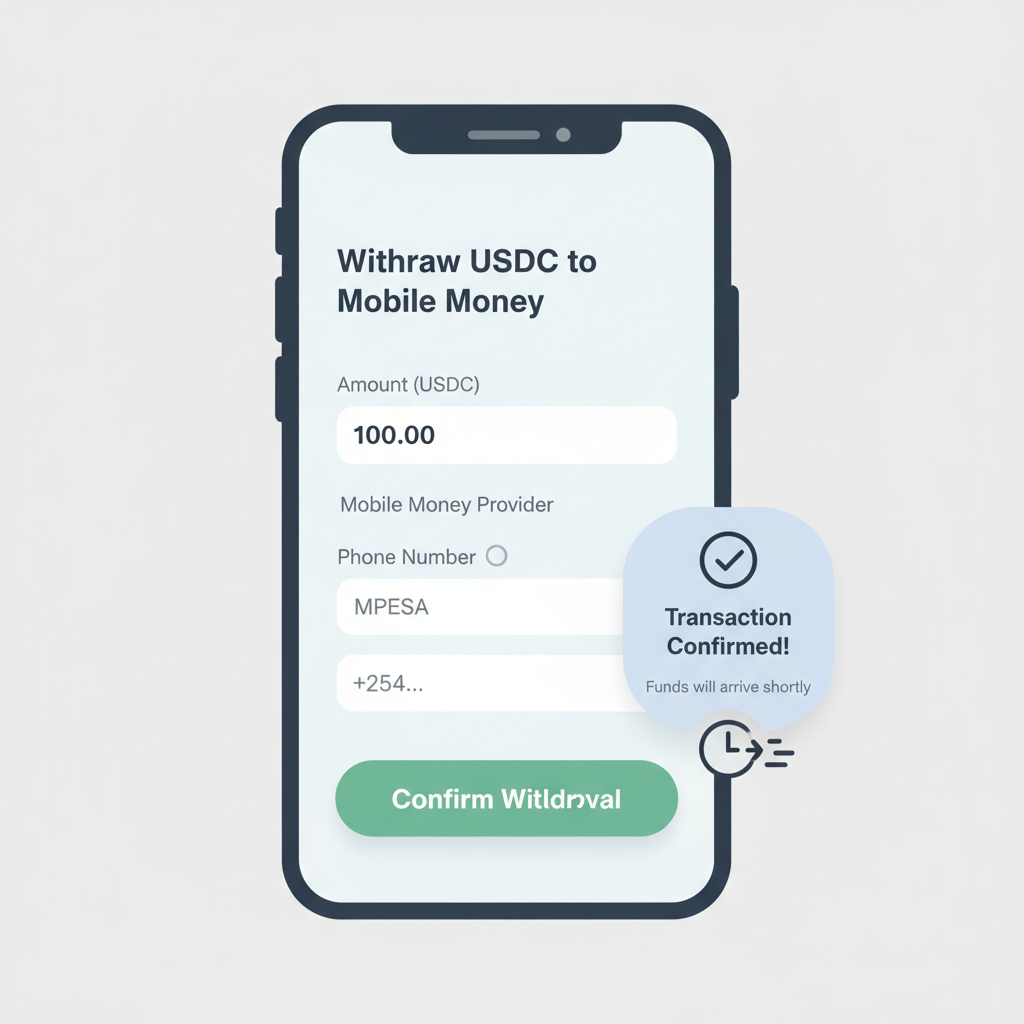

5 Strategic Steps to Launch USDC Savings on AfricaStableSave

This frictionless path democratizes high finance. A Kenyan mama mboga deposits shilling scraps daily; yields compound to fund school fees. Ghanaian traders hedge cedi swings mid-deal. AfricaStableSave optimizes each step, continent-tuned for low data use and offline confirmations.

Real-World Wins: Savers Gaining Ground Daily

Numbers tell tales sharper than anecdotes. Sub-Saharan stablecoin volumes surged 300% last year, per AInvest, as users fled hyperinflation. Yellow Card reports USDC remittances 70% cheaper than Western Union. Chipper Cash users in five countries now earn on idle balances, flipping idle cash into growers. Quona Capital spotlights mobile agent compatibility, extending reach to unbanked millions without forex queues.

Contrast this with bank inertia. South Africa's rates lag inflation; Zimbabwe's hypercycle renders deposits worthless. USDC sidesteps both, pegged firm via reserves. Fireblocks observes institutions piling in, validating retail moves. Even critiques like Center for Global Development's note stablecoins empower individuals, reshaping finance from the ground up.

Strategic allocation shines here. Diversify 30-50% of liquid savings into USDC via mobile for hedges plus yields. Monitor macro: Fed pauses could lift APYs further. AfricaStableSave's dashboard tracks it all, with alerts for optimal entry points.

Visionaries grasp the pivot: Africa's digital economy demands tools beyond colonial banking relics. Stablecoins, via mobile, forge self-reliant wealth builders. Freelancers shield gig pay; families secure remittances; entrepreneurs fuel growth. As adoption swells - Nigeria's P2P volumes hit billions monthly - yields compound not just capital, but continental momentum. Platforms like AfricaStableSave stand ready, bridging today’s volatility to tomorrow’s stability.

No comments yet. Be the first to share your thoughts!