Why African savers choose stablecoins

For many African households, saving in local currency feels like filling a bucket with a hole in the bottom. Currency depreciation and high inflation erode purchasing power faster than traditional savings accounts can compensate. In countries like Nigeria and Egypt, local bank interest rates often fail to keep pace with inflation, meaning real returns are negative. Stablecoins, primarily USD-pegged tokens like USDC and USDT, offer a way to hold value in a stable foreign currency without needing a foreign bank account.

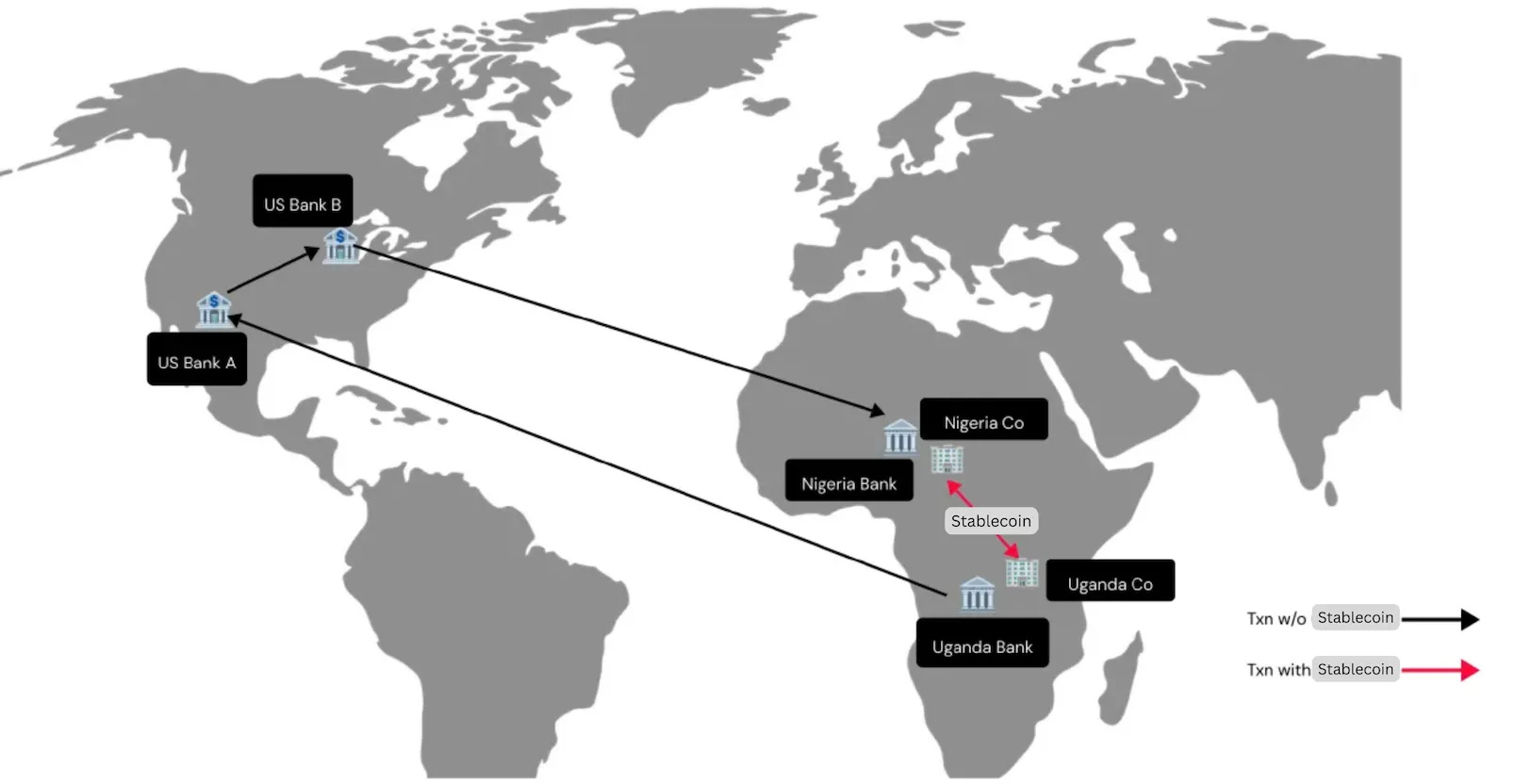

The practical appeal goes beyond simple preservation of value. With 70% of African countries facing foreign exchange (forex) shortages, accessing hard currency through traditional banking channels can be difficult, slow, and expensive. Stablecoins bypass these bottlenecks, allowing savers to move and store value instantly across borders. This accessibility is particularly vital for freelancers and small business owners who receive payments in dollars but need to hold them securely.

While the benefits are clear, the landscape is evolving. Regulators across the continent are urging faster frameworks to manage risks, acknowledging the traction stablecoins have gained as a practical tool for financial inclusion. For now, however, they remain a critical bridge for those seeking to protect their savings from local economic volatility.

7 Best African Stablecoin Savings Platforms for 2026

Navigating the African crypto landscape requires cutting through abstract promises to focus on platforms with verifiable regulatory compliance and real liquidity. This roundup evaluates seven specific stablecoin savings products, prioritizing official sources and concrete features over theoretical potential. We examine the actual tools available for 2026, ensuring you can compare tangible benefits and security measures across leading providers.

1. Yellow Card Pan-African Stablecoin Savings

Yellow Card operates as a dedicated bridge for African users seeking stable yield without complex DeFi interfaces. The platform focuses on seamless fiat-to-crypto onboarding across multiple jurisdictions, allowing users to deposit local currency and convert to stablecoins efficiently. Its infrastructure prioritizes regulatory compliance within local frameworks, making it a reliable entry point for newcomers who need a straightforward, regulated pathway into stablecoin savings without navigating decentralized protocols directly.

2. Binance Earn High Yield Options

Binance Earn aggregates diverse yield-generating products, offering users flexible choices between locked savings and flexible deposits. This platform leverages its massive liquidity to provide competitive APYs on USDT and USDC, catering to both conservative savers and those seeking higher returns through staking mechanisms. The interface simplifies the process of locking assets for fixed periods, ensuring that users can access their funds according to their specific liquidity needs while maximizing potential earnings across a broad spectrum of crypto assets.

3. Bybit Simple USDC Deposit Plans

Bybit distinguishes itself with straightforward USDC deposit plans designed for users prioritizing simplicity and transparency. The platform’s interface guides users through easy deposit processes, minimizing friction for those looking to park stablecoins in interest-bearing accounts. By focusing on USDC specifically, Bybit reduces volatility risks associated with other assets, offering a clean, predictable savings environment. This approach appeals to traders who want to maintain a stable portfolio base while earning passive income without navigating complex yield farming strategies.

4. KuCoin Earn Emerging Market Access

KuCoin Earn provides access to a wide array of emerging market opportunities, catering to users interested in diversified yield sources. The platform offers various earning products that span across different blockchain ecosystems, allowing users to explore niche opportunities beyond standard stablecoin savings. This diversity enables investors to spread risk across multiple assets and protocols, appealing to those who seek higher potential returns through a curated selection of innovative financial products available within the broader crypto economy.

5. Chipper Cash Local Fintech Savings

Chipper Cash integrates stablecoin savings directly into a familiar local fintech experience, bridging the gap between traditional banking and crypto. Users can move money across borders and convert to stablecoins within an app designed for everyday financial transactions. This integration lowers the barrier to entry for individuals who may not be crypto-native, offering a seamless way to save in stable assets while maintaining access to local payment networks. It represents a practical solution for cross-border savings and remittances.

6. Aave DeFi Protocol Stablecoin Yields

Aave offers a decentralized lending marketplace where users supply stablecoins to earn variable interest rates. This protocol allows African savers to access global liquidity pools without traditional banking intermediaries. The platform’s open-source nature ensures transparency, though users must manage their own private keys and understand smart contract risks associated with decentralized finance.

7. Compound Finance Decentralized Savings Rates

Compound Finance operates as an autonomous algorithmic money market, allowing users to supply assets and borrow against them. Its cToken system automatically adjusts interest rates based on supply and demand dynamics. For African users, this provides a permissionless way to earn yields on stablecoins, though the complexity of governance tokens requires careful navigation of protocol upgrades.

How to choose a secure savings platform

Evaluating a stablecoin savings platform requires a strict filter for regulatory compliance, security history, and withdrawal liquidity. In Africa, where currency volatility drives adoption, trusting a platform without verifying its legal standing is a significant risk.

Check if the platform holds a license from your country’s financial authority, such as the Central Bank of Nigeria or the Financial Services Authority in Kenya. Platforms operating without local registration may freeze accounts during regulatory crackdowns.

Review the platform’s history for hacks or exploits. Established platforms like Yellow Card or Bamboo have undergone multiple security audits. Look for transparent incident reports and proof of reserves rather than just marketing claims.

Before depositing large sums, execute a small test withdrawal to your local bank or mobile money account. This verifies that the platform processes payouts quickly and that fees do not erode your savings unexpectedly.

A platform’s ability to convert stablecoins to local currency during market stress is its most critical feature. Always prioritize platforms with deep liquidity pools and clear customer support channels for withdrawal issues.

Frequently asked questions about stablecoin savings

How are stablecoin earnings taxed in Africa? Tax treatment varies significantly across the continent. In Kenya, the Kenya Revenue Authority (KRA) treats crypto assets as chargeable assets, meaning capital gains tax applies to profits from selling stablecoins, while income from savings yields may be classified as business income. In Nigeria, the Federal Inland Revenue Service (FIRS) requires declaration of crypto holdings, though specific guidance on "savings" yields remains in development. Users should consult local tax professionals or official government portals to ensure compliance with current regulations in their specific jurisdiction.

Are stablecoin savings platforms safe for African users? Stability depends on the platform's reserve backing and regulatory status. Platforms like BitPesa (AZA Finance) operate with strict compliance frameworks in multiple African countries, while others may lack local oversight. As noted by The Conversation, heavy reliance on foreign-denominated stablecoins carries risks if the platform is not properly regulated. Always verify that the platform holds necessary licenses from local financial authorities, such as the Central Bank of Kenya or the Securities and Exchange Commission of Nigeria, rather than relying solely on the platform's own security claims.

Can I access stablecoin savings without a bank account? Yes, many platforms allow onboarding via mobile money or agent networks, bypassing traditional banking requirements. Services like Flutterwave and Chipper Cash integrate stablecoin features with local mobile money wallets, enabling users in Ghana, Kenya, and Nigeria to save and transact using just a phone number. This accessibility is a primary driver for stablecoin adoption in regions with limited banking infrastructure, though users should still verify identity (KYC) requirements, which often involve national ID verification.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!