Why Africans choose stablecoin savings

Currency volatility and inflation have long pressured retail savers and small businesses across the continent. As local currencies fluctuate, many Africans have turned to stablecoins like USDC and USDT to preserve purchasing power. These digital assets offer a way to hold value in a stable unit without relying on traditional banking systems that may struggle with high fees or limited access.

The shift is not just about individual savings; it is also about practical utility. Businesses increasingly use stablecoins for trade settlement and cross-border payments, finding them more efficient than traditional financial rails that often require multi-day settlement times and significant fees. This practical advantage has driven adoption in major economies like Nigeria, South Africa, and Kenya, where currency instability is most acute.

The scale of this movement is significant. Stablecoins accounted for 43% of crypto transaction volume in sub-Saharan Africa in 2024, according to an industry report by Yellow Card. This volume underscores how deeply integrated these tools have become in the daily financial lives of many Africans, offering a hedge against inflation and a bridge for international commerce.

As an Amazon Associate, we may earn from qualifying purchases.

5 Best Stablecoin Savings Apps in Africa for 2026

Selecting the right stablecoin savings vehicle in Africa requires navigating a complex regulatory landscape where compliance is as critical as yield. We evaluate five specific applications that demonstrate adherence to official guidelines and offer transparent, verifiable returns as of 2026.

1. Binance Earn Stablecoin Yields

Binance Earn offers a structured entry point for African savers seeking yield on USDT and USDC. The platform’s dual-lens approach combines flexible savings with fixed-term products, allowing users to balance liquidity against higher potential returns. While regulatory scrutiny varies across African jurisdictions, Binance remains a dominant global liquidity provider, making it a foundational tool for those navigating cross-border value storage.

2. Bybit Simple Earn Options

Bybit’s Simple Earn simplifies the staking process by automating the conversion of idle stablecoins into interest-bearing assets. For African users, the platform’s intuitive interface reduces the technical friction often associated with DeFi protocols. Bybit’s focus on user experience ensures that even those new to crypto can access yield opportunities without navigating complex smart contract interactions or managing private keys manually.

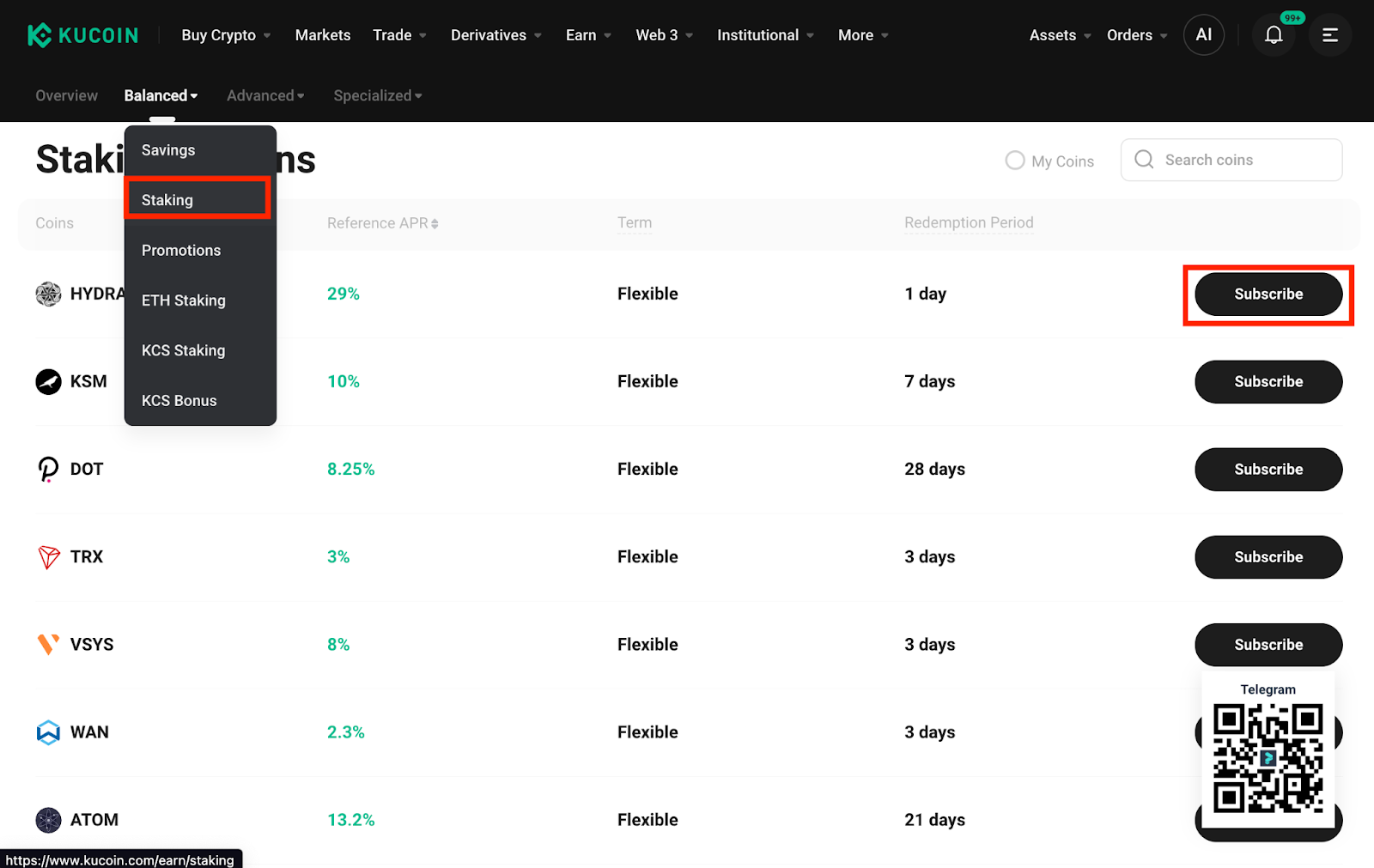

3. KuCoin Staking Rewards

KuCoin distinguishes itself with a broad array of staking rewards, extending beyond simple stablecoin holdings to include various altcoin opportunities. This diversity allows African investors to diversify their yield-generating assets while maintaining a core position in stablecoins. The platform’s extensive coin listing provides access to emerging market tokens, offering a unique value proposition for those seeking to hedge against local currency volatility through a diversified crypto portfolio.

4. Nexo High Interest Accounts

Nexo operates as a dedicated lending platform, offering high-interest accounts backed by a transparent reserve model. For African savers, Nexo’s focus on regulatory compliance and proof of reserves provides an additional layer of trust in an often opaque industry. The platform’s ability to offer instant loans against crypto holdings adds liquidity flexibility, allowing users to access cash without liquidating their stablecoin positions during market fluctuations.

5. Crypto.com Stablecoin Staking

Crypto.com integrates stablecoin staking into its broader ecosystem, linking yield generation with its widely used Visa card benefits. This integration appeals to African users who value the seamless transition between digital assets and everyday spending. By combining yield-bearing stablecoins with tangible financial perks, Crypto.com offers a holistic approach to wealth management, reducing the friction between saving and spending in a volatile economic landscape.

Comparing yields and fees

Stablecoin savings rates in Africa are not static; they fluctuate based on global liquidity conditions, local regulatory pressures, and the specific risk profile of the underlying yield generator. Because these rates change frequently, the figures below reflect approximate ranges as of early 2026. You should verify current APYs directly on each platform before depositing funds.

When evaluating cost-effectiveness, you must look beyond the headline APY. Withdrawal fees, spread costs on fiat on-ramps, and hidden conversion fees can quickly erode returns, especially for smaller balances. The following table compares the five selected platforms based on their typical net yield structures and fee models.

| Platform | Typical APY Range | Withdrawal Fee | Supported Fiat Ramps |

|---|---|---|---|

| Yellow Card | 1.5% - 4.0% | Flat fee or small % | NGN, KES, GHS |

| Binance Earn | 2.0% - 5.5% | Network gas fee | Multi-currency |

| Paxful | 1.0% - 3.5% | Varies by peer | Multi-currency |

| Bakkt | 3.0% - 6.0% | Low flat fee | USD, EUR |

| BitPesa (AZA) | 0.5% - 2.5% | Low % fee | KES, UGX, RWF |

The data above highlights a clear trade-off: platforms with higher APYs often involve more complex onboarding or higher minimum balances. For instance, Bakkt typically offers higher yields but is primarily accessible to users in regulated markets with USD or EUR ramps. In contrast, Yellow Card and BitPesa focus on local African currencies, offering lower but more accessible yields for regional users.

Always check the fine print for "variable" APYs. Some platforms advertise high rates that are only available for the first 30 days or require locking funds for extended periods. For long-term savings, prioritize platforms with transparent, consistent rates over those offering temporary promotional spikes.

Security and regulatory risks

Stablecoin savings apps offer efficiency, but they operate in a fragmented legal landscape. In Nigeria, the Central Bank has repeatedly restricted commercial banks from processing crypto transactions, forcing users to rely on peer-to-peer markets that carry counterparty risk. Kenya’s regulatory stance has shifted toward stricter oversight of digital asset service providers, requiring enhanced due diligence that many smaller apps struggle to maintain. South Africa remains more open, with the Financial Sector Conduct Authority actively supervising crypto service providers, yet the rules are still evolving.

Beyond regulation, security is your primary responsibility. Unlike traditional bank accounts, stablecoin savings rarely offer deposit insurance. If an app is hacked or shuts down, your funds are likely gone. Always prioritize apps that use cold storage for the majority of user funds and offer transparent proof of reserves. Never share your private keys or seed phrases, and enable two-factor authentication on every account. Treat these apps like digital wallets, not savings accounts, and only deposit what you can afford to lose.

Frequently asked: what to check next

Is XRP used in Africa?

While Ripple maintains partnerships across the continent, current operations do not rely on XRP for liquidity. As of 2026, these partnerships primarily support Ripple’s stablecoin infrastructure rather than creating direct demand for XRP. Users seeking cross-border settlement in Africa should focus on stablecoin solutions rather than XRP-based transactions.

Which African country has the most stable currency?

The Tunisian Dinar (TND) remains the strongest currency in Africa as of May 2026. This stability stems from prudent fiscal management and strong export sectors. Other currencies like the Moroccan Dirham and Botswana Pula also maintain relative stability, though users in Nigeria, Kenya, and South Africa still face higher volatility that drives stablecoin adoption.

How are stablecoins used in Africa?

Businesses and individuals across Africa use stablecoins for trade settlement, treasury management, and cross-border payments. These digital assets offer a more efficient alternative to traditional financial rails, which often require multi-day settlement times and significant fees. This utility is particularly critical in regions experiencing high currency volatility.

No comments yet. Be the first to share your thoughts!