Why stablecoin savings matter in 2026

For African investors, holding savings in local currencies carries a persistent risk of devaluation. In 2026, major economies like Nigeria and South Africa are driving the strongest growth in stablecoin demand as citizens seek a reliable hedge against local inflation and currency volatility [src-serp-6]. This shift is not merely speculative; it is a practical response to the erosion of purchasing power.

Regulated stablecoins are increasingly embedded in cross-border commerce, humanitarian aid, and small-business finance, offering a more accessible alternative to traditional USD banking [src-serp-7]. For the individual saver, this means access to a digital dollar that maintains its value while generating yield, bypassing the friction and high fees of conventional currency exchange.

The rise of yield-bearing stablecoin products in 2026 allows users to earn passive returns through tokenized Treasury exposure and on-chain lending. This transforms a stablecoin from a static store of value into an active savings vehicle, directly addressing the need for real returns in high-inflation environments.

Top platforms for stablecoin yields

Accessing stablecoin yields in Africa requires navigating a fragmented regulatory environment. Unlike traditional savings accounts, these products operate on blockchain infrastructure, meaning the platform’s legal standing and custody arrangements dictate the safety of your capital. In 2026, the primary risk is not just market volatility, but regulatory enforcement and jurisdictional exposure. Investors must prioritize platforms that have established clear compliance frameworks with local financial authorities or operate within recognized international regulatory sandboxes.

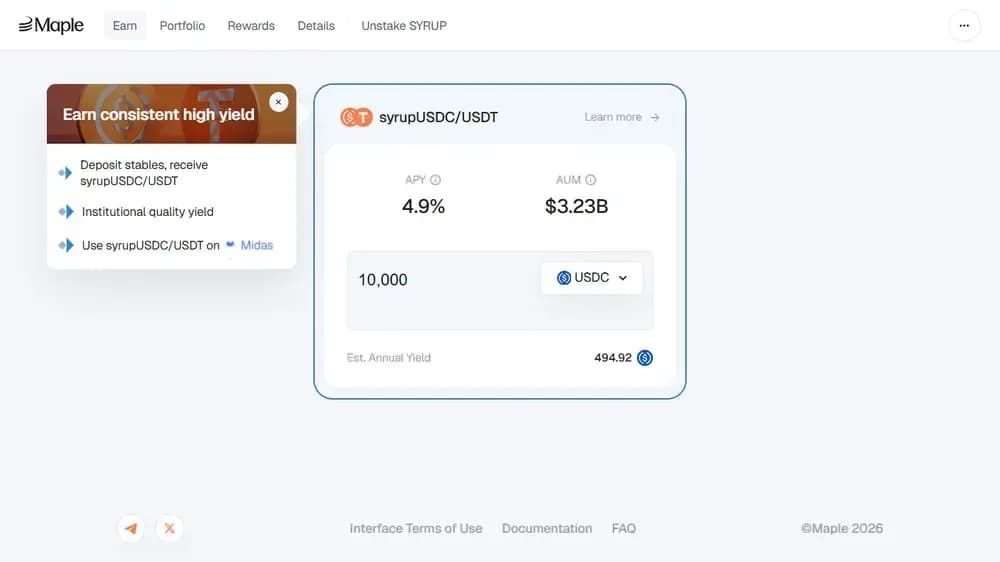

The following platforms have emerged as viable options for African investors seeking yield on USDC and USDT. These selections are based on their current operational footprint in African markets, supported by fiat on-ramps, and their adherence to evolving regional crypto guidelines. The table below compares these platforms on key metrics relevant to local compliance and accessibility.

Regulatory and operational considerations

The trend in 2026 shows a shift toward yield-bearing stablecoins linked to tokenized Treasury exposure or institutional cash-management systems. However, this innovation introduces counterparty risk. Platforms like Yellow Card have seen increased stablecoin adoption, often partnering with local banks to ensure fiat liquidity. This local integration is a critical safety feature for African investors, as it reduces reliance on volatile cross-border transfers. Conversely, global platforms like Binance or Bybit may offer higher yields but often operate in a regulatory gray area in certain jurisdictions, requiring users to perform their own due diligence on local enforcement actions.

When selecting a platform, verify if the platform holds any local licenses or partnerships. For instance, Luno operates with significant regulatory oversight in South Africa, providing a layer of institutional confidence. For investors in Nigeria or Kenya, Yellow Card’s localized compliance structure may offer a more secure pathway for entering and exiting stablecoin positions. Always check the latest regulatory updates from the Reserve Bank of your country, as frameworks are evolving rapidly.

As an Amazon Associate, we may earn from qualifying purchases.

Security best practices

Regardless of the platform’s regulatory standing, self-custody remains the gold standard for security. Consider using a hardware wallet for any stablecoin holdings that exceed your immediate liquidity needs. This separates your yield-generating assets from the operational risks of exchange platforms. Ensure your seed phrase is stored offline and never digitized. For ongoing transaction tracking, a dedicated ledger notebook can help maintain accurate records for tax purposes, especially given the complex reporting requirements in many African jurisdictions.

Regulatory landscape and safety

Stablecoin savings carry a unique risk profile: the asset is digital, but the regulations governing it are often traditional. For African investors, safety depends less on the platform’s marketing and more on its adherence to local central bank guidelines. In 2026, the regulatory environment remains fragmented, requiring investors to verify that their chosen platform complies with specific jurisdictional rules before depositing funds.

In South Africa, the Financial Sector Conduct Authority (FSCA) has moved toward a comprehensive regulatory framework for crypto-asset service providers. While stablecoins themselves are not yet explicitly banned, platforms offering savings products must navigate anti-money laundering (AML) and counter-terrorist financing (CTF) requirements strictly. Investors should look for platforms that are registered with the FSCA or operate under a recognized financial services license.

Nigeria presents a more complex picture. The Central Bank of Nigeria (CBN) has historically restricted banks from facilitating cryptocurrency transactions, though recent policy shifts have created openings for regulated digital asset exchanges. Platforms operating in Nigeria must ensure they have explicit approval to handle fiat on-ramps and off-ramps. Using unregulated platforms can expose users to frozen accounts or legal scrutiny, making verified compliance the primary safety metric.

Other key markets, such as Kenya and Ghana, are developing their own frameworks, often focusing on consumer protection rather than outright prohibition. The African Stablecoin Summit in late 2026 highlights this ongoing evolution, with regulators and bankers collaborating to standardize oversight. Until a unified continental framework emerges, investors must treat each market’s regulations as distinct and non-negotiable.

The trend toward yield-bearing stablecoins adds another layer of complexity. As platforms offer passive returns through tokenized Treasury exposure or on-chain lending, they assume additional regulatory obligations. Investors should ensure that the yield source is transparent and that the platform discloses how it manages regulatory risk in its home jurisdiction. If a platform operates in a regulatory gray area, the yield is likely a premium for unmanaged risk.

How to choose a secure platform

Selecting a stablecoin savings platform in Africa requires a rigid security framework. Regulatory status determines whether your capital is protected or exposed to total loss. You must verify licensing with official bodies such as the Central Bank of Kenya (CBK) or the South African Reserve Bank (SARB). Unregulated offshore entities operating without local compliance offer no legal recourse for African investors.

Liquidity depth dictates your ability to exit positions during market stress. Platforms must demonstrate sufficient reserves to handle redemptions without freezing withdrawals. Review the platform's reserve reports and audit trails to confirm that assets backing your stablecoins are held in segregated accounts. A platform that commingles user funds with operational capital poses an unacceptable counterparty risk.

Fees directly erode the yield generated by your savings. Compare the annual percentage yield (APY) against withdrawal fees, conversion costs, and network gas fees. High-yield offers often mask hidden costs in spread markups or inactivity fees. Calculate the net annual return after all deductions to ensure the platform aligns with your financial goals.

Check the platform's website footer or "About" section for registration numbers. Cross-reference these with official registries from the CBK, SARB, or the Nigerian Central Bank. Avoid platforms that claim "global licensing" without specifying a jurisdiction that covers your residency.

Require monthly or quarterly proof of reserves from independent third-party auditors. The platform must disclose the exact composition of its reserve assets, such as US Treasuries or cash equivalents. Do not accept self-reported attestations without external verification.

Review the platform's withdrawal terms for minimum hold periods or daily limits. A secure platform allows immediate access to your principal during normal market conditions. Check for any historical incidents of withdrawal freezes or delays.

| Feature | Regulated Platform | Unregulated Platform |

|---|---|---|

| Legal Recourse | Yes, under local law | None |

| Reserve Audits | Independent, monthly | Self-reported or none |

| Withdrawal Speed | Standard T+1 to T+3 | Subject to arbitrary freeze |

Frequently asked: what to check next

Which currency is the highest in Africa in 2026?

Market data identifies the highest-valued currency in Africa as the Tunisian dinar. However, high value does not always equate to liquidity or ease of use for cross-border digital transactions. For stablecoin users, the focus remains on peg stability rather than nominal exchange rates.

Where is stablecoin adoption growing fastest?

Demand for stablecoins is growing fastest in South Africa and Nigeria. These economies are driving the strongest growth in demand and are the most optimistic about digital asset integration, making them key markets for stablecoin savings platforms.

No comments yet. Be the first to share your thoughts!